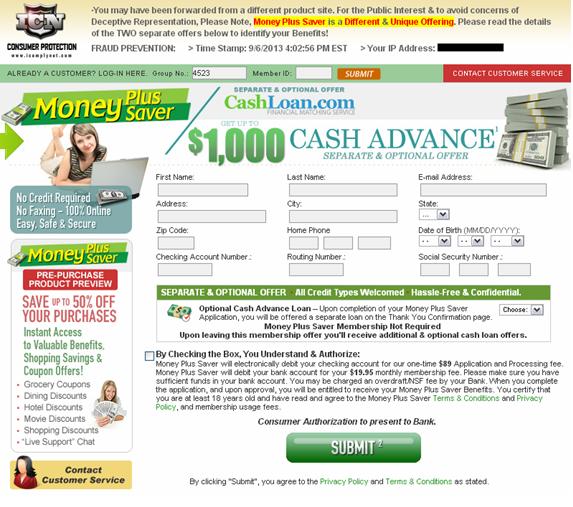

Here’s the catch: Money Plus Saver offers a members only discount program for instant savings of up to 50 percent on merchandise and services from over

250,000 retailers and a “separate and optional” offer of a cash advance of up to $1,000. Consumers who apply for payday loans are fighting mad when they open their bank statement and find themselves minus money in many ways: first, in the unexpected $89 application

and processing fee that shows up, next, in the unanticipated $19.95 continuing monthly membership fee, and finally, for some at least, returned check charges. Most have lost all patience with the company and just want to know how Money Plus Saver made off

with their money and how to get it back.

Money Plus Saver’s website lists several popular brands and advertises discounts on groceries, shopping, recreation, entertainment, dining, automotive services, and more. The terms and conditions state

that the company will electronically debit your bank account for a one-time application and processing fee of $89 and an additional $19.95 monthly afterwards for the membership. Users cannot submit an application to become a Money Plus Saver member without

providing sensitive information including social security number and checking account information. Many individuals have reported that they have incurred unauthorized charges to their accounts from Money Plus Saver and their attempts to obtain refunds have

been ignored.

We’ve received an influx of

complaints within the last year. Most of the complainants have never heard of Money Plus Saver and only find out about the company when their accounts are charged. Many get hit by the unauthorized charges after applying for payday loans or cash advances

on other websites. At the time they applied for the advance, they provided their banking information. One consumer says, “If we’re looking for a payday loan, that means we have no money. Why in the world would we pay $89 to get it?” Another complainant who

applied for but was denied a loan says, “I didn't get the loan, but these people took $89.00 out of my checking account without my knowing about it.”

And the problems only seem to mount for complainants when they attempt to recover the unauthorized fees. Although the company’s website claims you may cancel the $89 processing fee if you cancel the membership within three days of your submission or three

days after completing the application, complainants say they’ve been unable to get refunds. Many customers are unaware that they signed up for any membership, so for them it’s impossible to cancel within the three days. Also, in order to obtain a refund, Money

Plus Saver requires that the customer provide a copy of the bank statement showing that the funds have been deducted, along with the bank statement date, within five days after receiving the statement. Customers say they’ve done this, some multiple times,

but haven’t received a refund. One Florida customer says Money Plus Saver’s unauthorized withdrawals caused her bank account to be overdrawn.

So far, we’ve received 97 complaints about Money Plus Saver. And so far, Money Plus Saver has failed to respond to our office regarding any of the complaints, although three complainants tell us that they finally received a refund. Money Plus Saver’s failure

to address the customers complaints, along with its volume of complaints and the seriousness of the complaint allegations, have earned the company an

F rating with us.

The cash advance offer on Money Plus Saver’s website is offered by

CashLoan.com, an F-rated company that operates under several other DBA’s, including EDebitPay, LLC. In February 2011, EDebitPay, LLC, its principals, and some of its subsidiaries entered into a $2.2 million

stipulated settlement agreement with the Federal Trade Commission (FTC) to settle charges that they made unauthorized debits from consumers’ bank accounts and deceptively marketed prepaid debit cards and

short-term loans.

Kim’s advice: Don’t get caught. Watch out for hidden fees, terms and conditions. Protect your information and only give your personal account, banking, and other sensitive information to trusted individuals that you have thoroughly researched.

Consider the following if you’re considering a cash advance or payday loan:

- While payday loans and cash advances can sound tempting, they can be a financial burden and nightmare if you use a fraudulent company, or if you can’t pay them back. Consider other options first.

- If other options are not available or feasible and you’re sure you want to apply for a cash advance or payday loan, research the business or lending source. Start by

checking for a reliability report on the Business Consumer Alliance website. Also, do an Internet search for the business, along with the words “scam,” “complaints,” or “reviews” to find out if others

have had a negative experience with the company. Make sure you are able to contact the lender and that you have a physical location for the business. It may be best to consider local lenders who provide the services as opposed to companies that offer the services

online. Shopping online for loans may expose you to privacy and security risks.

- Consider the fees associated with the loan.

By law, payday lenders must disclose the cost of the loan, the finance charges (which can range from $15 to $30 per $100 borrowed), and the annual percentage rate (APR), or cost of credit on a yearly basis. The average APR for these loans is typically 300%,

but can be more. Shop around for the offer that costs the least.

- Check that the lender is licensed by contacting the

state’s bank regulator or

attorney general’s office.

If you are considering entering a membership program or discount offer:

- Check out the offer by utilizing our

“Check out a Business” feature.

- Read and understand all terms and conditions, policies, fees, refund and cancellation provisions. If you are reviewing the offer online, make sure there are no pre-selected boxes already checked that would enroll you into an automatic membership, which

more than likely will have recurring fees. If you do not agree with the terms, do not go further with the offer.

- Maintain good records and obtain or print copies of all documents.

- If possible, pay by credit card. While this method is not incident proof, if you don’t receive the services or there are billing disputes, you may be able to file a dispute with your financial establishment to recover fees and charges.

- Verify with the company that there is a cancellation policy and get a copy of the cancellation procedures. Contact some of the phone numbers or send an email to ensure that someone responds. If you are unable to contact customer service, it may be in your

best interest to seek services elsewhere.